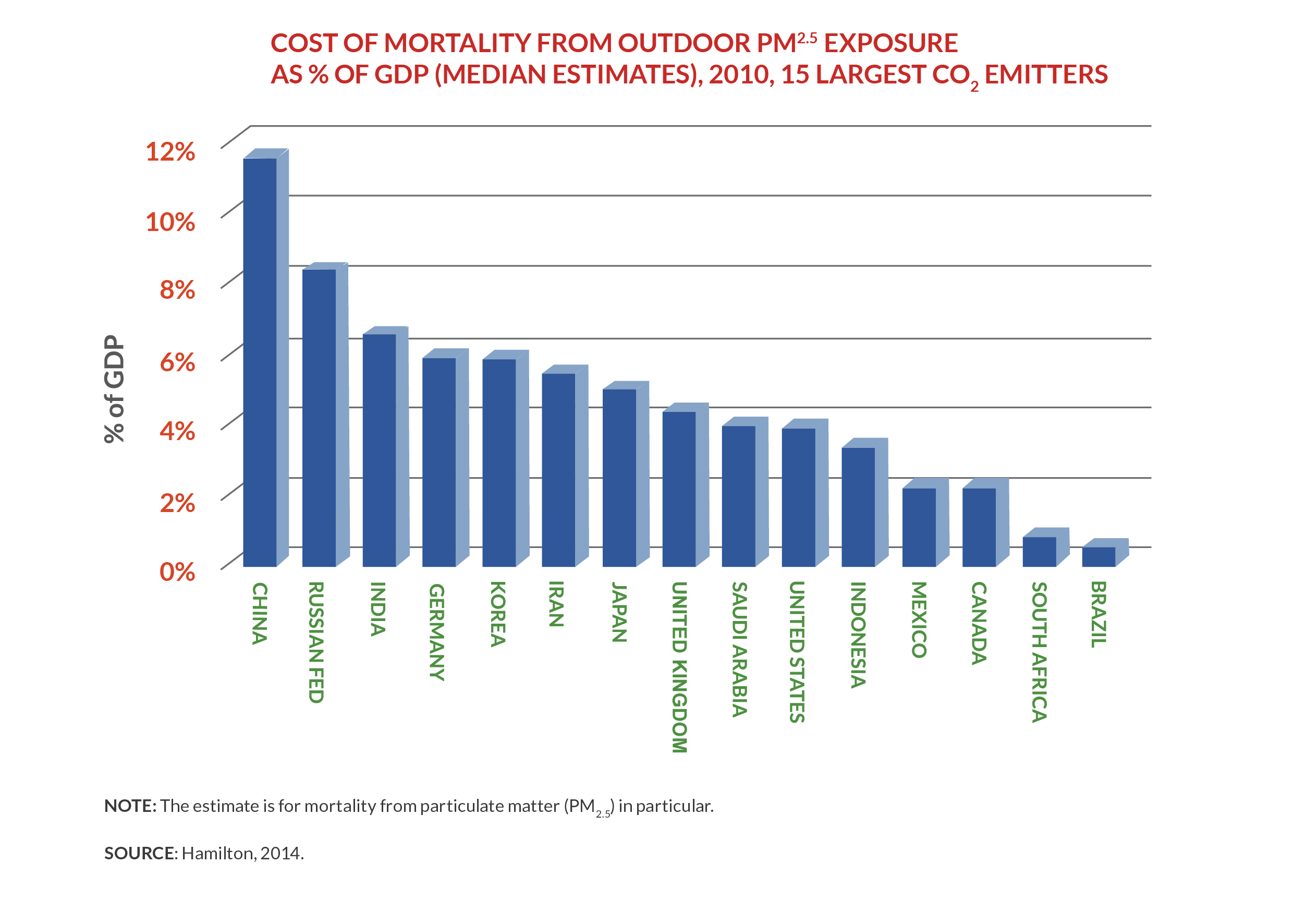

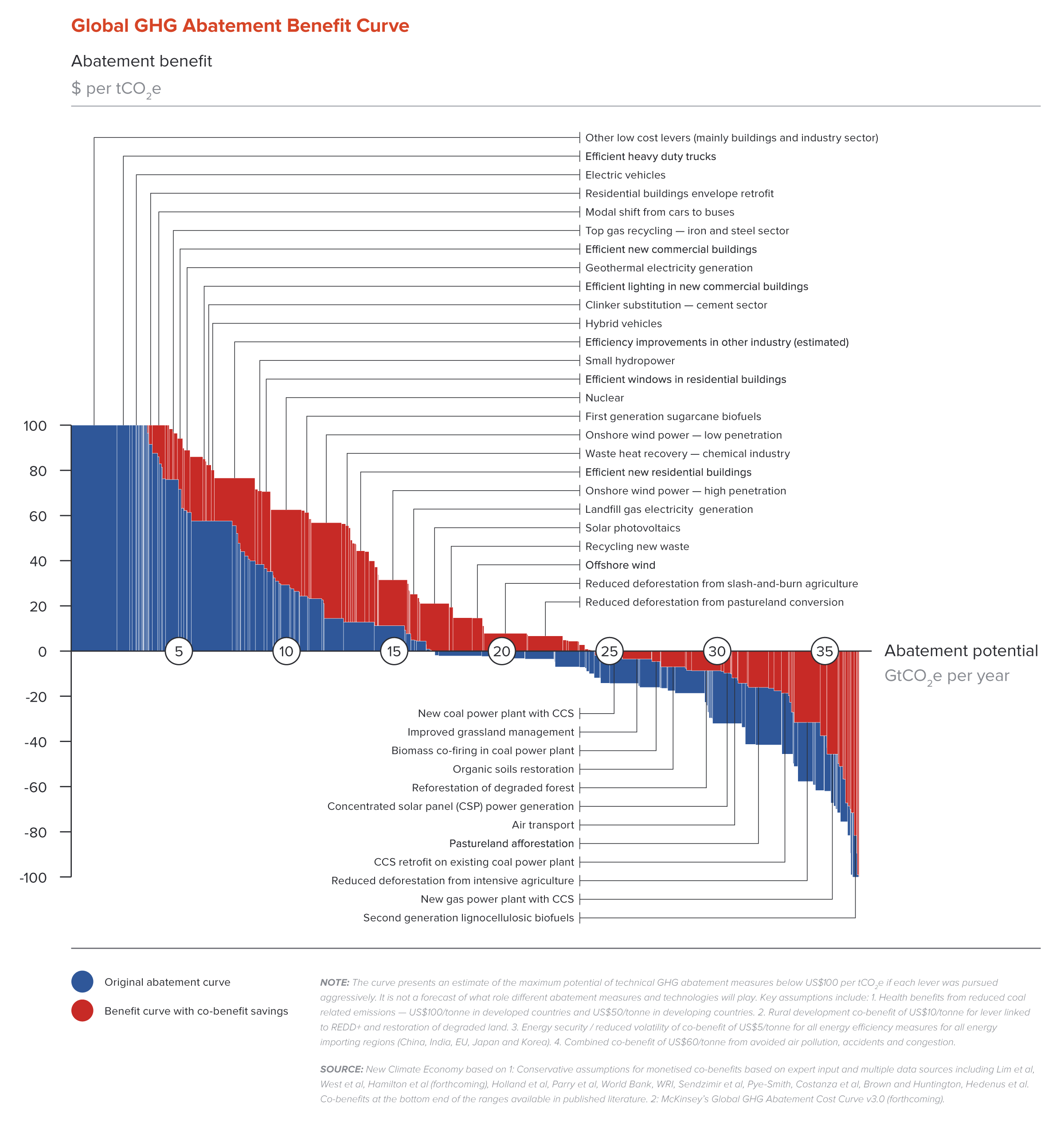

It is sometimes useful to express the monetary value of health damages from local air pollution per tonne of CO2 emitted from fossil fuel combustion. With some caveats, this indicator also provides an estimate of the potential health benefits per tonne of CO2 abatement. A recent study calculates the median value of such health benefits for the 15 largest CO2 emitters at US$73 per tonne of CO2 abated in 2010. 51 Illustrating the significance of these numbers, they are more than double US government estimates for the climate benefit of reducing CO2 emissions. The US Interagency Working Group on Social Cost of Carbon estimated this climate benefit at US$32 per tonne of CO2 abatement in 2010. 52 Adding the median US$73 benefit from reduced air pollution in the 15 largest emitters would triple the overall benefit from cutting carbon emissions. Furthermore, and importantly from the perspective of policy-makers, the air quality benefits are enjoyed in the near term; accrue locally, mostly to the country itself; and are more certain compared with climate change benefits.

This discussion of avoided local air pollution provides a specific example of the importance of accounting for multiple benefits when evaluating climate actions. In practice, it would be important to look carefully at how the size and time paths of the various benefits and costs differ across countries. Many aspects of the links between greenhouse gases and local air pollutants, including synergies and trade-offs, need to be better understood.

From the perspective of policy-makers, an important complication is that there may be alternative policies that generate a different set of benefits. For example, a significant volume of local air pollution can be mitigated by so-called “end of pipe” methods that do not reduce GHG emissions, such as sulphur scrubbers fitted to the smokestacks of power plants. If countries pursued more ambitious air pollution reduction targets, however, then “end of pipe” methods are unlikely to be enough. It would still then be necessary to adopt methods that also reduce GHG emissions.

One of the few model-based studies to estimate the scale of GHG reductions from ambitious air pollution policies considered an illustrative scenario in which countries sought to reduce premature air pollution-related deaths in 2050 by 25% compared with 2005. This ambitious air pollution target also yielded large GHG reductions by 2050, falling by 38% in the OECD, 61% in China and 42% in India, compared with a baseline without mitigation policies.53

Fossil fuel combustion, especially from coal, is the major source of PM pollution in China, causing severe smog and haze problems in major cities. In 2013 only three Chinese cities met a so-called “Grade II” air quality standard (equivalent to less than 35 micrograms of PM per cubic metre). Research for the Commission suggests that even with the most advanced end-of-pipe technologies, only 50% of Chinese cities would be able to achieve the Grade II air quality standard by 2030. Instead, it will be necessary to adopt upstream methods which replace fossil fuels to ensure that most Chinese cities meet these air quality standards. Such transformational policies would also generate GHG reductions and help China peak its emissions by around 2030.54

In a full cost-benefit analysis, policy-makers could compare the total multiple benefits (net of costs) of a GHG mitigation policy against those of an air pollution reduction policy. An optimal policy would seek a combination of GHG and air pollution measures, to maximise total multiple benefits net of costs. One study finds that an optimal, combined policy achieves air quality benefits as large as an air pollution-only policy, while also achieving climate benefits larger than in a GHG-only mitigation policy. 55 The net total benefits of the combined policy are larger than either of the separate policies. Clearly, this is an important policy theme which deserves to be explored more thoroughly going forward.

Scope for reforms: some qualifications and limitations

We have used the term “win-win” to refer to the potential for reforms which tap multiple benefits by tackling numerous market and policy failures. It is important to describe some qualifications and limitations.

First, such reforms still entail costs and various trade-offs. To illustrate, consider a common example of a “win-win” reform, to reduce fossil fuel consumer subsidies. Such a reform can reduce fiscal pressures, improve economic efficiency, and yield multiple benefits in reduced local air pollution and GHG emissions. However, it also entails costs, including human costs and loss of output that occur as workers and equipment in some sectors become unemployed for some time, before finding employment in rising sectors. Costs and trade-offs exist in all cases, and need to be carefully examined and dealt with in undertaking reforms.

Second, there is the “problem of the second best”. In an economy with multiple imperfections, an attempt to correct one imperfection could reduce rather than increase overall welfare. 56 Here there are no easy formulas. Each situation would need to be analysed carefully on its merits and policy might need to proceed through step-by-step experiment and learning-by-doing to discover the right combination of instruments to advance overall welfare over the course of time.

Third, there are often deep political economy or institutional reasons why governments do not undertake reforms to eliminate a market or policy failure. Government failure can lead to reforms themselves introducing new distortions or inefficiencies that leave the country worse off than before. Such failures can occur, for example, when governments are mainly responding to influential special interests or rent-seekers; lack credibility with the public; or are mainly driven by short-term political objectives. As a result, the hard and poorly understood problem of improving governance and institutions is an essential element of reform strategies to tackle development and climate objectives.

Some of these limitations may represent daunting challenges for reform. But this should not discourage a well-considered, bold and persistent effort to act, given the potential for immense gains in human welfare and poverty reduction, and the severe climate losses that could accompany inaction.

Is climate action too costly?

There is never a good time for major change, especially one which involves complex political dynamics and deep institutional reform. To make progress, it is crucial to examine the many thoughtful and reasoned concerns about potential adverse effects of climate action. Here we briefly discuss some of the main concerns that are sometimes raised against taking immediate action on climate.

The most widely held concern is that climate action is simply too costly. In developing countries, an important concern is that attempts to tackle climate change will derail their immediate and overriding objective of rapid economic growth and poverty reduction. In all countries there are concerns about potential effects on employment and competitiveness in the global economy.

In evaluating such concerns, it is important to take into account the full costs and benefits of all available options. Sometimes a policy may appear too costly because not all its benefits are accounted for. The appropriate metric for judging an economic policy is its impact on overall welfare. In this report, we have tried to focus on policies and reforms which improve overall national welfare, productivity and efficiency, and which also help reduce climate risk.

Often the analysis focuses only on the costs to a particular sector – for example, the pollution or carbon-intensive industries in the economy – while ignoring broader effects on the welfare of the public at large, such as improvements in health from reduced local air pollution. A lack of environmental regulation is in effect a form of subsidy to highly polluting firms at the expense of a less healthy public, and less polluting firms. Environmental policy improves overall economic efficiency and welfare by removing the implicit subsidy for polluting firms, and by causing a reallocation of resources towards cleaner activities.

The exclusive use of GDP as a yardstick to measure the welfare effects of reform can also be misleading. The effect on GDP might include a potential loss in measured output of goods and services, but not other types of changes in welfare, for example in improved health. Policy-makers should supplement GDP effects with estimates of broader welfare gains, which can also be estimated in monetary terms, albeit sometimes only roughly. 57

If policy-makers do want to focus solely only on GDP effects, however, several points are relevant. First, the assumptions of models used to make such estimates need to be carefully scrutinised. Models often start from the assumption of an economy where resources are already efficiently allocated, for the good reason that we do not yet know how to model the real world of multiple imperfections and numerous inefficiencies. The effects of reform are therefore judged against the assumed starting point of an efficient economy. Such results, while interesting, need to be used cautiously as a guide to policy, when one is judging the results of reform versus non-reform in a highly imperfect and inefficient world.

Second, as Chapter 5: Economics of Change discusses in more detail, the estimated global costs of efficient climate policy, such as a carbon tax, are usually rather limited, perhaps of the order of 1–4% of global consumption in 2030, with a median value of 1.7%, according to the IPCC’s review of recent studies. 58 Such costs are fairly small in relation to the much larger underlying increase in consumption that would occur by 2030. Assuming consumption growth of 3% in 2015–30, a little less than average world GDP growth since 1980, a median 1.7% cost would represent a delay of about six months in achieving the level of consumption that would have been reached in 2030 without climate policies. This does not seem an excessive insurance premium to pay to start reducing the possibility of dangerous climate change. Note that the cost estimates discussed here do not include the kinds of multiple benefits discussed above, nor the benefits of averted climate damages. Such model-based cost estimates can also be significantly reduced by optimal recycling of revenues from a carbon tax – for example, to cut labour and capital taxes.

Third, adopting a somewhat costlier option today may make sense in a highly uncertain world where there is a value in keeping options open and avoiding getting locked into courses that might turn out to be very expensive in the future. This point is especially relevant when building large, long-lived infrastructure such as transport networks or power systems.

Fourth, the cost-benefit ratio for climate action depends greatly on the international context. There is a disincentive for governments to undertake reforms with climate trade-offs, because climate action creates a global public good. The benefits from a single country’s efforts to reduce GHG emissions will accrue to all countries. But if countries act together to reduce emissions, then the climate benefits for each country are much larger. Chapter 8: International Cooperation explores approaches for enhancing global cooperation on climate action, including the need for climate finance to help developing countries make progress.

Will climate action lead to loss of competitiveness?

The particular focus here is the potential harm caused by climate action to the international competitiveness of a country’s industries. The concern is that higher costs relative to foreign competitors will cause a shift in pollution-intensive industries to other countries with less strict regulation.

Empirical studies have found this relocation effect to be small, where it is found at all, reflecting the fact that pollution abatement costs are only a small proportion of total costs in most industries. In addition, environmental regulations can induce firms to increase innovation as a way to offset such higher costs. Governments may nevertheless consider providing carefully designed transitional assistance to vulnerable sectors. 59

Developing countries may worry that environmental policies will hinder their industrialisation. They may argue that it is better to “grow dirty and clean up later”. Developing countries indeed face numerous coordination and market failures that may hamper structural change and the success of tradable goods industries, which, even if they are polluting, might well be important for long-term growth and structural change. As noted earlier, “growing dirty” implies subsidising polluting industries at the expense of less polluting firms and the public at large, who suffer from pollution and ill-health. Lack of environmental regulation can then be a form of industrial policy to support polluting tradable sectors, one that is relatively easy to implement, as it does not make heavy demands on institutional capacity. Developing countries should, however, be able to reach a better outcome if they combine tighter environmental policy with more focused government interventions in support of structural change, backed by a sustained effort to strengthen institutional capacity. To encourage such approaches, developed countries could consider providing greater flexibility under international trade rules to accommodate well-managed industrial policy interventions by developing countries. 60

Will climate action hurt the poor?

Whether climate actions such as removing fossil fuel subsidies or a carbon tax are regressive (having a greater relative negative effect on the poor) depends to some extent on country circumstances. There is some evidence that they tend to be regressive in developed countries, but less so in developing nations, where the upper and middle classes may be the major consumers of energy. 61 Regardless of this relative impact, policy-makers are concerned about the absolute impacts of higher energy prices on the poor. Well-designed and targeted safety net measures to help vulnerable groups are an essential element in the political economy of reforms.

Will climate action cost jobs?

Linked to concerns about competitiveness are fears that environmental policies will significantly increase unemployment. Others have argued that such policies will, on the contrary, be a source of “green jobs”.

A good starting point is to note that the aim and effect of environmental and climate policies is to induce a substitution between different types of production and consumption, away from more polluting to less polluting activities. There is no special reason to expect any overall net job gains or losses from this adjustment. While there is a clear finding in the research that any overall employment effects of environmental policies are small, there is no consensus whether those small effects would be positive or negative. 62 (See Chapter 5: Economics of Change for further details).

There will, however, be changes in the numbers and types of jobs across and within economic sectors, and there could be significant adjustment issues, as workers need to move from declining to expanding sectors, firms and job types. This will require specific policies to shape a just transition. The amount of such “churn” or job destruction and job creation linked to climate mitigation is expected to about 0.5% of total employment – quite small compared with the overall “churn” that normally occurs in a market economy. Job effects may be larger in economies with larger labour market imperfections. The recycling of revenues from carbon taxes or emissions trading schemes can mitigate job impacts. For example, studies suggest that recycling of carbon tax revenues to reduce labour market taxes could offset or more than offset all adverse impacts of climate action on employment. 63

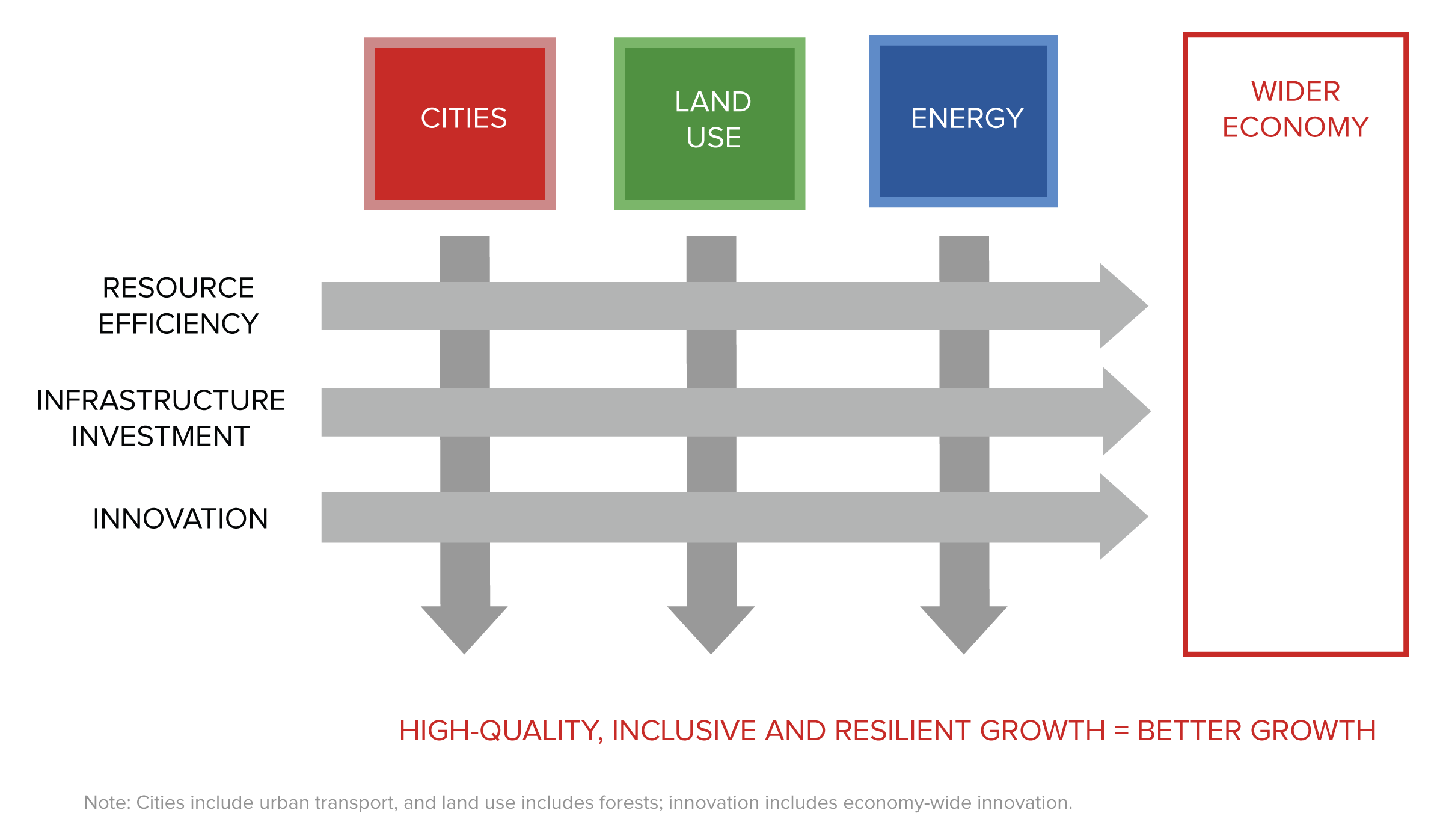

Enabling change through resource efficiency, investment and innovation

Policy efforts to promote rapid development and tackle climate risk will draw upon and work through three fundamental mechanisms or drivers of change that affect every sector of the economy: efficiency of resource use; investment, particularly in infrastructure, and innovation.

Resource efficiency

The discussion in the preceding section has stressed the presence of numerous market and policy failures which result in an inefficient allocation of resources and lower levels of welfare. Fossil fuel consumer subsidies are an important example. They result in multiple resource misallocations, including excessive capital and labour employed in pollution-intensive sectors. Within sectors, firms use more fossil fuel- and pollution-intensive methods of production. Consumers’ shopping baskets are biased towards fossil fuel- and pollution-intensive goods and services. There is too much local air pollution, damaging citizens’ health and productivity, and too high GHG emissions, storing up climate risks for the future. 64

Reforms of fossil fuel subsidies, discussed in more detail in Chapter 5: Economics of Change, can stimulate improvements in efficiency of resource use in all these dimensions. Various instruments can improve resource efficiency by tackling market failure, including price-based instruments such as carbon taxes or emission trading schemes, as well as regulations and standards, and information-based instruments, among others.

Infrastructure investment

Infrastructure refers to the large interconnected physical networks – transport, communications, buildings, energy, water and waste management – that provide critical services to and raise the productivity of the economy as a whole. Investment in infrastructure is a fundamental mechanism to expand the productive capacity of the economy.

Recent economic research has provided much evidence on the high, economy-wide returns to efficiently allocated and well-managed infrastructure capital. 65 As Chapter 6: Finance indicates, almost US$90 trillion infrastructure spending (in constant 2010 dollars) is projected to be needed in 2015–30 across the cities, land use and energy systems, especially in developing countries. Ensuring that this new infrastructure does not lock countries into a high-carbon path, but rather supports the transition to a low-carbon economy, is expected to have a net additional cost of about US$4 trillion. The latter does not include longer-term operational savings in a low-carbon transition, as a result of burning less fossil fuels.

Increased investment is a means of increasing consumption in the future. When the economy is operating at full capacity, it will, in general, demand some sacrifice of present consumption. But that is hardly the case in large parts of the world today, which are continuing to operate at below their potential output in the wake of the Great Recession. Investment is hardly constrained by a shortage of savings, as suggested by low long-term real interest rates. Yet world gross fixed investment relative to GDP has fallen to around 21% in the years since the crisis, the lowest level in 50 years, entirely due to a fall in developed countries, to around 19%. 66 The present macroeconomic context thus provides a particularly favourable opportunity for policies to foster stronger global growth through increased infrastructure investment, including in low-carbon systems. 67 Chapter 6: Finance further explores policy approaches to boosting infrastructure spending on low-carbon assets, in particular through institutional innovations to encourage private-sector financing and engagement.

Innovation

Innovation and technological progress are by far the most important drivers of long-term growth in productivity and output. 68 It is also becoming clear that innovation is likely to be the most important long-term driver to mitigate climate change, in particular by fostering new technologies that can supply energy that is not only clean but also cheap and abundant. The latter condition is critical if the world is to satisfy rapidly growing energy demand in developing countries while also abating GHG emissions and climate change.

A broad definition of innovation includes not only cutting-edge research and development (R&D), but also deployment, diffusion and adoption of existing technologies, the latter being especially important in developing countries. It includes not only development of new products and production processes, but also institutional innovation and new methods of business organisation, marketing and distribution. Relatively simple innovations can have enormous impacts: the introduction of the humble shipping container revolutionised global freight transport and is estimated to explain a 700% increase in industrialised country trade over 20 years. 69

There is a large role for public policy to foster innovation. As Box 3 above indicates, innovation is subject to its own specific market failures, such as knowledge spillovers, network externalities and asymmetric information. These failures mean that private incentives alone are generally inadequate to generate an optimal amount of innovation. Market incentives for climate-friendly innovation are further reduced by the failure to price externalities related to GHG emissions, which boost the profitability of polluting relative to clean technologies. The introduction of environmental pricing on fossil fuels would improve the price incentives for innovators to seek out new cleaner technologies, in addition to improving the efficiency of existing resource allocation.

Chapter 7: Innovation discusses various public policy responses, including public-sector R&D, fiscal incentives, public procurement, intellectual property rights and other instruments. Innovation market failures also provide a rationale for policies tailored to promote innovation in clean technologies more specifically. That is because market failures affecting innovation also promote path dependence. 70 The large existing base of research in fossil fuel technologies, for example, has given them a large “head start”, and favours further innovations on that path. This path dependence, or bias in favour of existing dirty technologies, could hinder or prevent the creation of a clean energy innovation complex and path that might otherwise generate new clean technologies that are ultimately even cheaper than their dirty competitors.